Millions of pensioners across the United Kingdom rely on the State Pension as a key source of income in retirement. For many households, it provides the financial foundation that helps cover everyday expenses such as groceries, energy bills, transport and housing costs.

Each year, the government reviews pension payments to ensure they remain aligned with economic conditions. These adjustments are designed to help pensioners maintain their purchasing power as the cost of living changes over time.

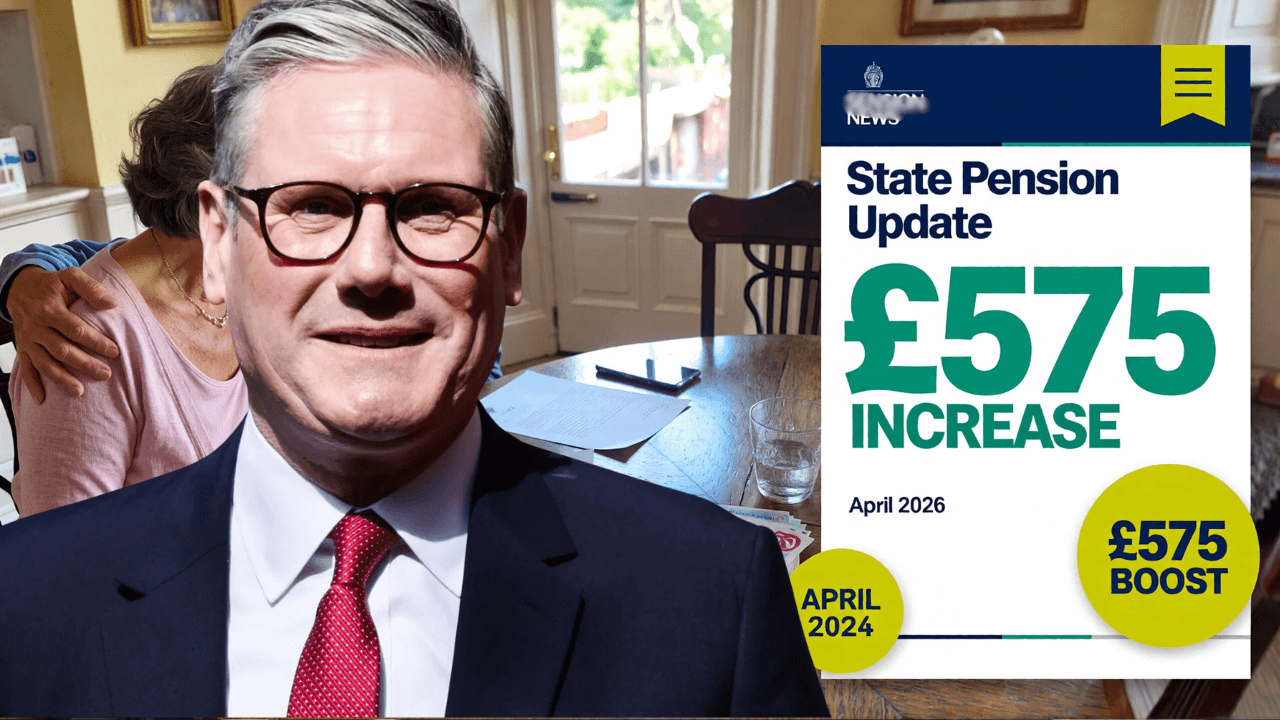

Recently, the UK government confirmed that the State Pension will increase again in April 2026. The announcement has attracted significant attention because it represents one of the most important financial updates for older residents.

The increase has been confirmed by the Department for Work and Pensions, which manages pension payments and a wide range of welfare programmes across the country.

For pensioners and those approaching retirement age, understanding how the increase works and when it will appear in payments can help with financial planning for the coming year.

Why the State Pension changes each year

The State Pension is designed to provide long‑term financial support for people who have reached retirement age. However, because the cost of living changes over time, pension payments are reviewed regularly.

In the UK, the amount pensioners receive can increase annually based on economic indicators. This system helps ensure that pension income does not lose value as prices rise.

Adjustments are usually announced before the start of the new financial year and implemented in April.

These changes are part of the government’s broader strategy to support retirees and maintain stability within the pension system.

Understanding the UK State Pension

State Pension is a regular payment from the government that provides income to individuals who have reached the official retirement age and have made sufficient National Insurance contributions during their working lives.

The amount someone receives depends on their National Insurance record. People who have contributed for enough qualifying years typically receive the full State Pension.

Those with fewer qualifying years may receive a partial payment based on their contributions.

The State Pension therefore reflects a person’s working history and contributions to the national insurance system.

How the £575 increase works

The figure of £575 represents the approximate annual increase that many pensioners may see in their total State Pension income after the adjustment takes effect.

Rather than being paid as a single lump sum, the increase is usually distributed across weekly pension payments throughout the year.

This means that pensioners will see a slightly higher payment each week once the new rates begin in April.

Although the exact amount varies depending on an individual’s pension entitlement, the overall increase can help offset rising living costs.

For many retirees, even a modest increase can make a meaningful difference to household finances.

When the new pension payments will start

The updated State Pension rates will begin from April 2026, which coincides with the start of the UK financial year.

However, pensioners may notice the increase at slightly different times depending on their payment schedule.

State Pension payments are typically made every four weeks directly into a recipient’s bank account.

Once the new rates take effect, the increased amount will appear automatically in the next payment cycle.

Because the update is applied automatically, pensioners do not need to submit any new application to receive the increased payment.

The role of National Insurance contributions

Eligibility for the full State Pension depends on a person’s National Insurance contribution history.

During their working life, individuals contribute to the National Insurance system through employment or self‑employment.

These contributions help fund several government programmes, including pensions and certain benefits.

Generally, individuals need a minimum number of qualifying years to receive the full pension amount.

Those with fewer qualifying years may still receive a reduced payment based on their record.

Additional support available for pensioners

In addition to the State Pension, some retirees may qualify for other forms of financial assistance.

One of the most important programmes for pensioners with lower incomes is Pension Credit.

This benefit helps increase the income of pensioners whose retirement income falls below a certain threshold.

Receiving Pension Credit may also open the door to other types of support, including assistance with housing costs or council tax.

Because of this, it is important for pensioners to explore all the benefits available to them.

The impact of rising living costs

Many households across the UK have experienced rising living costs in recent years.

Energy prices, food costs and other essential expenses have increased for many families.

For pensioners who rely on fixed retirement income, these changes can place pressure on monthly budgets.

Annual pension increases are therefore an important way to help retirees manage these financial challenges.

While no increase can completely eliminate the impact of rising prices, adjustments help ensure that pension payments continue to provide meaningful support.

Budgeting with pension income

For retirees, careful financial planning is often an important part of managing everyday expenses.

Many pensioners create monthly budgets that take into account housing costs, food, transportation and healthcare.

Understanding when payment changes will occur can help retirees plan ahead and adjust spending if necessary.

Financial advice services and community organisations often provide guidance to help pensioners manage their finances effectively.

These resources can be especially useful for people navigating retirement income for the first time.

Why pension updates attract attention

Changes to the State Pension always attract significant public interest because millions of people depend on these payments.

For retirees, pension income represents stability and security after years of employment.

Announcements about increases therefore receive widespread attention from pensioners, policymakers and financial experts.

Public discussions about pensions often focus on how to balance long‑term financial sustainability with the need to support older citizens.

These debates highlight the central role that pensions play within the UK’s social support system.

Planning for retirement in the future

While the State Pension provides an important foundation for retirement income, many financial experts encourage people to supplement it with additional savings or workplace pensions.

Private pensions and personal savings can help provide extra financial security later in life.

Planning early allows individuals to build additional resources that can support their lifestyle during retirement.

Combining different sources of income can help retirees maintain financial stability even as economic conditions change.

Key points pensioners should remember

The State Pension will increase in April 2026

Many pensioners may see around £575 more per year

Payments will rise automatically without a new application

Eligibility depends on National Insurance contributions

Additional support such as Pension Credit may also be available

Final thoughts

The confirmation of a State Pension increase for April 2026 represents an important update for retirees across the United Kingdom. As living costs continue to evolve, adjustments to pension payments help ensure that older citizens receive financial support that reflects current economic conditions.

For millions of pensioners, the State Pension remains a vital source of income that supports everyday living. With the upcoming increase set to take effect in the new financial year, many retirees will be watching closely as the updated payments begin appearing in their accounts.