In recent months, many pensioners across the United Kingdom have reported receiving official letters regarding their savings and tax status. These notices, issued by the UK’s tax authority, have sparked questions among retirees who are trying to understand whether their savings could affect their tax obligations or benefit eligibility.

The letters come from HM Revenue and Customs, the government body responsible for administering the UK tax system. HMRC routinely sends communications to taxpayers when financial records indicate that certain thresholds or reporting rules may apply.

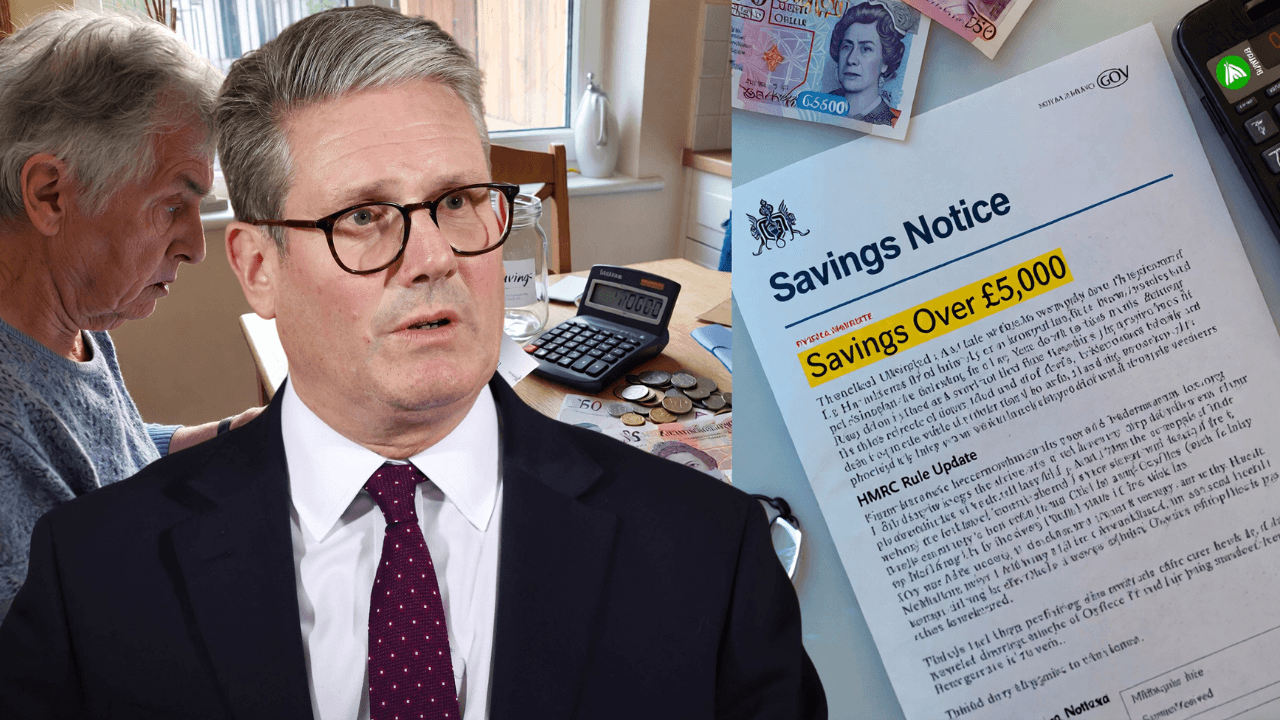

For pensioners with savings of £5,000 or more, these notices are often designed to clarify how savings interest and other forms of income should be reported. While receiving such a letter can sometimes cause concern, it does not necessarily mean that someone has done anything wrong.

Instead, the communication usually serves as a reminder about how savings and tax rules operate in the UK.

Why HMRC sends savings notices

HMRC collects and processes financial information from a wide range of sources, including banks, employers and pension providers. These records allow the tax authority to monitor income levels and ensure that individuals are paying the correct amount of tax.

When savings accounts generate interest, that interest counts as income under UK tax law. If HMRC’s records suggest that someone may have earned taxable interest, the agency may send a letter explaining how the rules apply.

In many cases, the notice is simply informational and does not require immediate action.

For pensioners, these letters often relate to how savings interest interacts with other sources of income such as pensions.

Understanding the role of savings interest

Savings accounts generate interest when banks pay customers for holding money in their accounts. Although interest rates vary, even modest savings can produce taxable income depending on the amount earned during the year.

For example, someone with £5,000 or more in savings may begin to see interest payments accumulate over time. While the amount may be relatively small, HMRC still considers this interest part of an individual’s total income.

The tax treatment of this interest depends on how much income a person receives from other sources.

For pensioners who rely primarily on the State Pension, savings interest may sometimes push total income closer to the taxable threshold.

The importance of the personal allowance

One of the key features of the UK tax system is the personal allowance. This allowance represents the amount of income a person can earn before paying income tax.

For many pensioners, their total income may fall below this threshold, meaning they do not owe income tax even if they receive savings interest.

However, when multiple income sources are combined—such as pension payments, private pensions and savings interest—the total may exceed the allowance.

In such cases, HMRC may review the situation and inform the individual of any tax obligations.

Receiving a letter does not necessarily mean tax is due, but it may indicate that HMRC is checking whether the correct tax code is being applied.

How savings affect pensioners

Savings can provide an important financial cushion during retirement. Many retirees rely on savings accounts to cover unexpected expenses or supplement their pension income.

However, the presence of savings can sometimes influence how income is assessed for tax purposes.

Interest earned from savings is treated as income, which means it contributes to a person’s overall taxable earnings.

For pensioners who also receive income from private pensions or investments, the combined total determines whether tax applies.

Understanding this interaction helps retirees manage their finances more effectively.

The role of the Personal Savings Allowance

In addition to the personal allowance, the UK tax system also provides a Personal Savings Allowance.

This allowance allows individuals to earn a certain amount of savings interest without paying tax on it.

The exact amount depends on the taxpayer’s income level and tax band.

For many pensioners, this allowance means that small amounts of interest from savings accounts remain tax‑free.

Because of this rule, many people who receive HMRC notices discover that they do not actually owe additional tax.

The letter simply explains how the system works.

Why pensioners are receiving letters now

HMRC regularly updates its records as banks report interest earned by account holders.

If the tax authority notices that someone’s financial records show savings interest or income that has not been fully accounted for, it may issue a letter.

These letters are often part of routine checks designed to ensure the tax system operates correctly.

Because many pensioners rely on savings accounts, they may be among the groups most likely to receive such communications.

However, receiving a notice does not automatically indicate that tax will be owed.

How pensioners should respond to HMRC letters

If a pensioner receives a savings notice from HMRC, the first step is simply to read the letter carefully.

In many cases, the letter explains why HMRC is contacting the recipient and what information the agency is reviewing.

Sometimes no action is required at all.

If the letter requests additional information, the recipient may be asked to confirm income details or update personal records.

Anyone who is unsure about the contents of the letter can contact HMRC directly for clarification.

Official guidance can help ensure that any necessary steps are completed correctly.

Avoiding scams related to tax letters

Whenever news spreads about HMRC communications, scammers sometimes attempt to take advantage of the situation.

Fraudulent emails or text messages may claim to be from HMRC and request sensitive personal information.

These messages can look convincing but are often designed to steal financial details.

It is important to remember that genuine HMRC letters are usually sent through official channels and will not request confidential information through unexpected messages.

If someone receives suspicious communication claiming to be from HMRC, they should verify it through official contact methods.

Managing savings during retirement

For pensioners, maintaining savings can be an important part of financial security. Having money set aside can help cover medical costs, home repairs or other unexpected expenses.

However, it is also helpful to understand how savings interact with tax rules.

Reviewing bank statements and interest payments periodically can help retirees track how much income their savings generate.

If interest income increases significantly, it may be worth reviewing tax obligations to ensure that everything is reported correctly.

Financial advisers can also provide guidance on managing savings in a tax‑efficient way.

The role of financial awareness

Understanding how savings, pensions and taxes interact can help retirees avoid confusion when they receive official letters.

Many pensioners are surprised to learn that savings interest counts as income for tax purposes.

Staying informed about tax allowances and financial rules can help individuals make better decisions about managing their money.

Government communications are often designed to provide information rather than create problems for taxpayers.

By reading these letters carefully and responding appropriately when necessary, pensioners can ensure their financial records remain accurate.

Key points pensioners should remember

HMRC monitors savings interest as part of income reporting

Savings interest may count toward taxable income

The personal allowance determines how much income is tax‑free

The Personal Savings Allowance protects small amounts of interest

HMRC letters often serve as routine information notices

Final thoughts

The recent notices sent to pensioners with savings of £5,000 or more highlight how the UK tax system keeps track of different types of income. While receiving a letter from HMRC may initially cause concern, these communications are often part of routine checks designed to ensure taxpayers are paying the correct amount.

For retirees, the key is understanding how savings interest interacts with pension income and tax allowances. By staying informed and reviewing financial records regularly, pensioners can manage their savings confidently and ensure they remain compliant with UK tax rules.