The personal tax allowance has long been one of the most important elements of the UK tax system. It determines how much income individuals can earn each year before paying income tax. For millions of workers, retirees and savers, this allowance directly affects how much money they keep from their earnings.

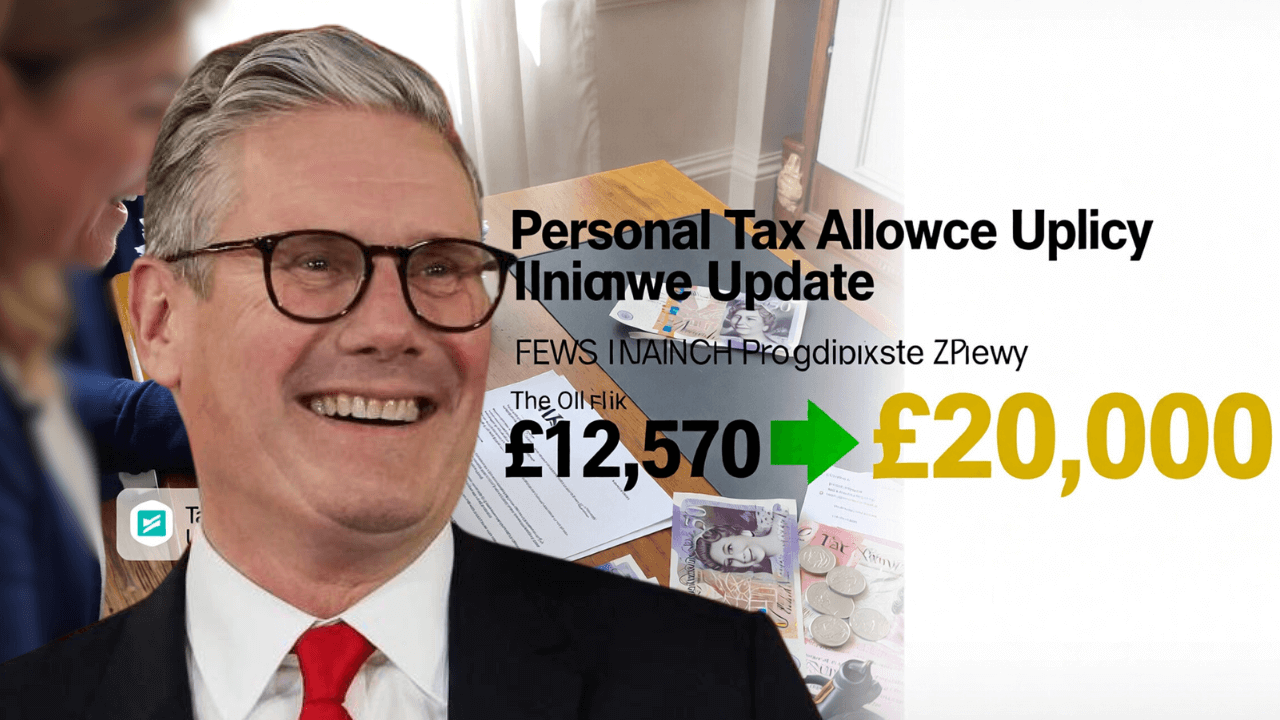

Recently, discussions have intensified around proposals to raise the personal tax allowance from £12,570 to £20,000. The idea has gained attention because such a change could significantly increase the amount of income people can receive before tax applies.

Although the proposal has sparked debate among policymakers and economists, it highlights the broader conversation about taxation, household finances and the rising cost of living. For many people across the UK, understanding what the proposal means and how it could affect them is increasingly important.

What the personal tax allowance is

The personal tax allowance is the amount of income individuals can earn each tax year before they begin paying income tax. This allowance applies to most types of income, including wages, pension payments and certain investment earnings.

The system is administered by HM Revenue and Customs, the government body responsible for collecting taxes and ensuring that the tax system operates fairly.

Currently, the standard personal allowance is set at £12,570 for most taxpayers. Once income exceeds this amount, the remaining portion is taxed according to the relevant income tax bands.

For basic‑rate taxpayers, income above the allowance is typically taxed at 20 percent.

Why increasing the allowance is being discussed

The proposal to raise the allowance to £20,000 has gained attention because it would represent one of the largest increases in the tax‑free threshold in decades.

Supporters of the idea argue that increasing the allowance would help households cope with rising living costs. Higher food prices, energy bills and housing expenses have placed financial pressure on many families in recent years.

Allowing people to earn more before paying tax could help increase disposable income and improve financial stability for many households.

However, such a change would also reduce government tax revenue, which is why discussions around the proposal involve careful economic analysis.

How the change could affect workers

If the personal allowance were raised to £20,000, millions of workers could benefit from lower tax bills.

For someone earning slightly above the current allowance threshold, the increase could mean paying significantly less tax each year.

For example, individuals earning between £12,570 and £20,000 currently pay income tax on the portion above the existing allowance. Raising the threshold would remove tax liability on that income range.

For many households, this could result in hundreds or even thousands of pounds in additional annual income.

Potential benefits for pensioners

Retirees could also benefit from a higher tax‑free allowance.

Many pensioners receive income from the State Pension along with workplace pensions or savings interest.

Because pension income counts toward taxable income, some retirees currently pay tax when their total income exceeds the personal allowance.

If the allowance increased to £20,000, more pensioners might find that their entire income falls below the tax threshold.

This could reduce tax obligations for retirees and allow them to keep more of their pension income.

How tax allowances affect household budgets

Tax allowances play a crucial role in shaping household finances.

When the allowance increases, people keep more of their earnings before tax is applied. This additional income can help cover everyday expenses such as food, energy bills and housing costs.

For families living on tight budgets, even modest changes to tax rules can make a noticeable difference.

Because the personal allowance applies to a wide range of taxpayers, any change to the threshold affects millions of people simultaneously.

Concerns about government revenue

While raising the tax‑free allowance could benefit households, economists also highlight potential challenges.

Income tax represents one of the largest sources of government revenue in the UK. This revenue helps fund essential public services including healthcare, education and infrastructure.

A significant increase in the allowance could reduce the amount of tax collected each year.

To compensate for this reduction, policymakers might need to adjust other taxes or spending priorities.

This is why discussions about tax policy often involve balancing household support with long‑term fiscal sustainability.

The role of the Treasury in tax policy

Decisions about tax allowances and national tax policy involve several government departments.

The UK Treasury plays a central role in shaping fiscal policy and determining how tax rules evolve over time.

Policy proposals and economic forecasts are carefully reviewed before any major changes are introduced.

While political discussions may highlight potential reforms, formal policy changes typically occur through annual budgets or major fiscal statements.

These processes ensure that tax policy decisions are evaluated in the context of the wider economy.

How tax bands interact with the allowance

The personal allowance is only one part of the UK income tax structure.

Once income exceeds the allowance, different tax bands apply depending on how much a person earns.

The main income tax bands include:

Basic rate

Higher rate

Additional rate

Each band applies a different percentage of tax to income above specific thresholds.

If the personal allowance increases, it effectively shifts the starting point for taxation higher, reducing the portion of income subject to tax.

The broader debate about tax reform

The proposal to raise the allowance to £20,000 forms part of a broader debate about tax reform in the UK.

Some economists argue that increasing the tax‑free threshold could simplify the tax system and reduce financial pressure on lower‑income households.

Others suggest that targeted benefits or adjustments to tax credits may provide more focused support for those who need it most.

These discussions reflect the challenge of designing a tax system that balances fairness, economic growth and public spending needs.

Why taxpayers should stay informed

Tax policies can change over time as governments respond to economic conditions and public priorities.

For individuals and families, staying informed about tax rules can help with financial planning and budgeting.

Understanding how allowances, tax bands and deductions interact allows taxpayers to make better decisions about savings, employment and retirement planning.

Even small changes to tax rules can have meaningful effects on household finances.

Planning finances under changing tax rules

Whether tax allowances increase or remain the same, financial planning remains important.

Many people benefit from reviewing their income sources, tax codes and savings strategies regularly.

Workers may consider pension contributions or savings plans that maximise tax efficiency.

Retirees may review how their pension income interacts with tax allowances.

Taking a proactive approach to financial planning can help individuals adapt to changing tax rules and make the most of available allowances.

Key points to remember

The personal tax allowance determines how much income can be earned before paying tax.

The current allowance is £12,570 for most taxpayers.

A proposal suggests increasing the threshold to £20,000.

Higher allowances could reduce tax bills for workers and pensioners.

Policy changes would require careful evaluation by government authorities.

Final thoughts

Proposals to raise the personal tax allowance from £12,570 to £20,000 have sparked considerable interest because of their potential impact on household finances across the United Kingdom.

While such a change could significantly reduce income tax for millions of people, it would also require careful consideration of government revenues and economic policy.

For taxpayers, the key takeaway is that the personal allowance remains a central feature of the UK tax system. By understanding how this allowance works and staying informed about potential changes, individuals can better plan their finances and navigate the evolving landscape of taxation in the UK.